Could You Retire a Millionaire?

Investing in Index Funds

![]() Over the past couple of decades, investing in index funds has become increasingly popular. This means that rather than investing in a mutual fund or ETF that has a manager picking stocks, you have a fund company that automatically buys shares in a stock market index.

Over the past couple of decades, investing in index funds has become increasingly popular. This means that rather than investing in a mutual fund or ETF that has a manager picking stocks, you have a fund company that automatically buys shares in a stock market index.

For example, think of the S&P 500; an index fund based on this stock market grouping would automatically buy shares in every one of the companies in the index. How many of each would depend on how much the fund is investing.

Advocates of index funds say their funds usually do better than the alternatives because of lower costs. An index fund is involved in what’s known as passive investing, rather than active investing. In other words, a fund manager is not actively picking stocks, instead, a computer simply picks an equal number of stocks or bonds for every name in the index.

In any case, folks at the Motley Fool have transcribed a podcast called Everything You Need to Know About Index Funds, and it does have a lot of information (but I’ll let you decide if it’s everything you need to know). Here’s the lead-in:

“On this edition of Industry Focus: Financials, join The Motley Fool’s Gaby Lapera and Jordan Wathen as they discuss everything you need to know about investing in index funds, why they’re so popular, and why they may be a great investment for your retirement portfolio.”

Does investing in index funds appeal to you?

Capital Gains Tax Information

This article was originally published in 2016, but the issues it covers remain relevant.

This article was originally published in 2016, but the issues it covers remain relevant.

Toward the end of every calendar year, something important happens. No, not Santa and not snow tires. For mutual fund investors, it’s the time of year to start thinking about capital gains tax information–and action.

Sometime in December many mutual funds begin distributing accumulated capital gains to unit holders (investors). In most cases, that will involve a cash injection into your account. Which is a good thing, except if your mutual fund is not in a registered account, then you may have to pay taxes on the windfall, if we can call it that.

An article posted at Investopedia warns not only that distributions are coming, but that they may be higher this year (again, a good thing if not for the taxes),

“Russel Kinnel, Morningstar’s director of manager research, recently issued a warning to investors and advisors regarding capital gains distributions. He told InvestmentNews that “we’ve seen continued stock market appreciation and redemptions for active funds. Even if we’d seen a more or less flat year, we might see an uptick because the gains from previous years are still around.””

If you need more capital gains tax information, get in touch with your financial advisor, your broker, or get Googling.

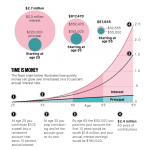

Could You Retire a Millionaire?

That’s a good question, and the answer could be yes, you could retire a millionaire, especially if you start saving and investing early enough.

That’s a good question, and the answer could be yes, you could retire a millionaire, especially if you start saving and investing early enough.

You see, the key is compound interest. That’s interest on interest, and the longer your time frame, the better it works. An article in the OC Register, Focus: What you need to know to retire a millionaire, takes us through a quick and easy drill on the subject.

I generally agree with most of the information in the article, but would draw your attention to the claim you need 85% of your pre-retirement income. Many financial advisers argue that 60%, or even 50%, will work for many retirees because they’ll spend less when they retire. No more commuting costs, lower clothing costs, no lunches in the cafeteria, and so on.

The other thing to consider is what you want to do after retiring. If you plan to travel in luxury then you’ll need more money than you would if you plan to garden and read books after you stop working.

Every one of us will have a different perspective on retirement, and understanding that is just as important as understanding the financial mechanics. Save on!